Progressing Towards an Equal and Growing Latin America

Progressive tax reform is a historically underutilized fiscal policy tool, but informed persons should demand structural changes to the distribution of income, starting at the local level and adopting potentially beneficial policy changes across the developing world.

by Brian Balduzzi, MBA ’18

Introduction

Tax experts have long proposed using taxation to alleviate inequality and redistribute income within developing countries (Lustig, 2016). Recent scholarship suggests that adopting and implementing a personal income tax system for developing countries, modeled after that of developed countries, ignores some of the key differences between these two types of countries (Gordon & Li, 2009). In what follows, the use of personal income taxation is reviewed to determine some of the potential benefits, and limitations, of this policy tool in minimizing or alleviating income equality within such country.

Section I: Measuring Income Inequality in Emerging Markets

Income equality is key to economic growth within developing countries. The distribution of capital may encourage higher productivity and consumption, leading to a higher gross domestic product (GDP) (Bird & Zolt, 2008). Income equality and the redistribution of income is also important for political stability within a country as it can minimize crime and alleviate poverty (Bird & Zolt, 2005), which stifles growth (Berens & von Schiller, 2017).

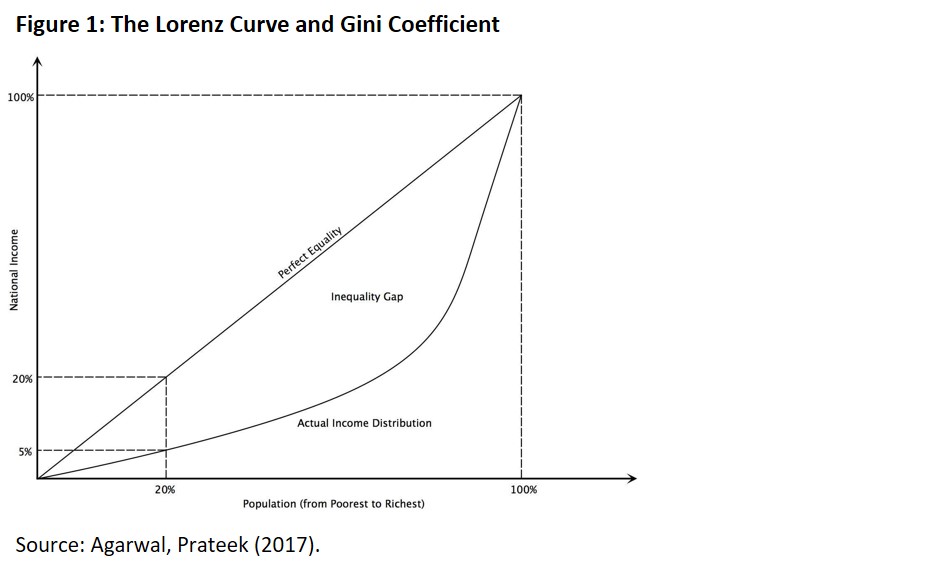

To measure and compare domestic income inequality, many economists and politicians have relied on the Gini coefficient (Haughton & Khandker, 2009). This most common measurement of inequality enables policy-makers to consider the current socio-economic landscape, as well as to determine the impact of domestic policy changes on income inequality. The World Bank explains the coefficient as ranging from 0, complete equality, to 1, complete inequality, taken as the measure of the area between the Lorenz curve and the line of equality (Figure 1) (Haughton & Khandker, 2009).

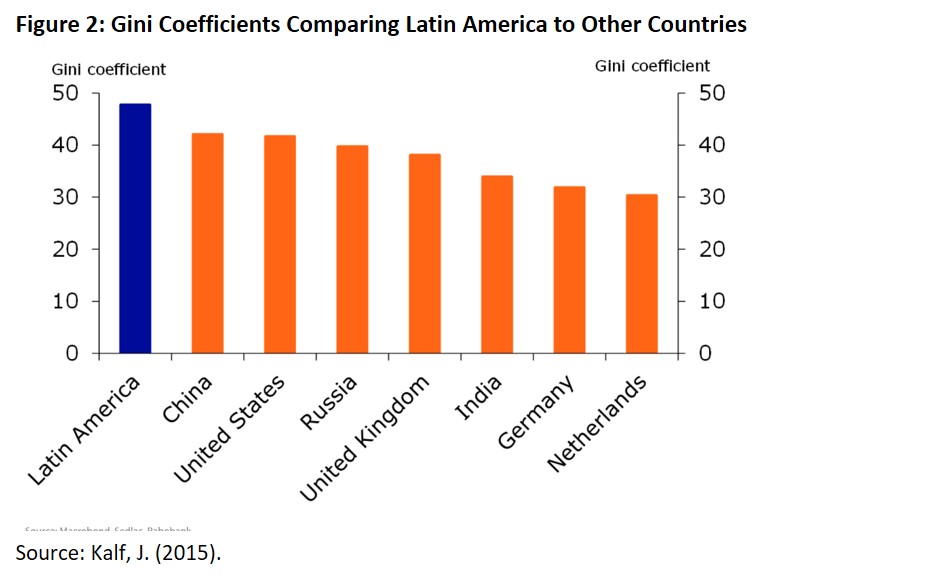

Using data collected by the World Bank, we can estimate the Gini coefficient for a select group of Latin American countries, based on their status as developing countries and on the availability of its income equity data, including: (1) Argentina, (2) Brazil, (3) Columbia, and (4) Peru (Figure 2) (World Bank, 2015).

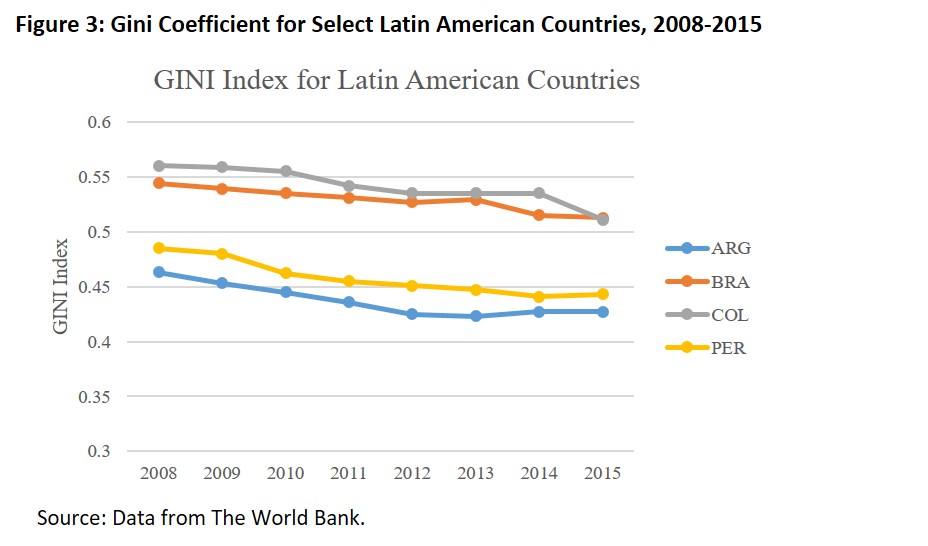

We see that, notwithstanding, their status as among the more unequal economies in the world, their Gini coefficients are largely declining (Figure 3).

This data shows that policy plays a critical role in the alleviation of the disparate income distribution within these countries.

Section II: Understanding the Personal Income Tax System Within Latin America

Economists and politicians have proposed combating income inequality through changes to tax policy and procedures. Domestic tax systems serve many purposes: (1) to raise revenue to fund government activity, (2) encourage or discourage certain types of behavior, and (3) correct market imperfections. Taxes can also distribute resources among different classes of citizen, and stands as a reflection of a government’s political and philosophical choices.

First, while some economists argue that income taxes account for only between 5-10% of tax revenue and less than 1% of GDP, their redistributive purposes act as an important driver for economic activity (Bird & Zolt, 2005). And yet, this approach may lead some citizens to pursue income in the “shadow economy,” which can escape the collection of tax reporting and withholding (Bird & Zolt, 2005). Latin America continues to have one of the largest informal economic activity in the world (Jiménez, 2011). Bird and Zolt (2011) argued that, within developing countries, “taxing the agricultural sector and small businesses is difficult due to the lack of administrative capacity,” as a result of which the costs can outweigh the benefits.

Second, tax policy may also affect social drivers within a country and is a reflection of a society’s values vis-à-vis its citizenry. While personal income tax accounts for a small portion of tax revenue, it is one of the most public redistributive forms supporting key social drivers such as “improvements to access to healthcare, education, and employment opportunities” (Bird & Zolt, 2005). For developing countries, these resources and reallocations are essential for a country’s political stability and economic growth.

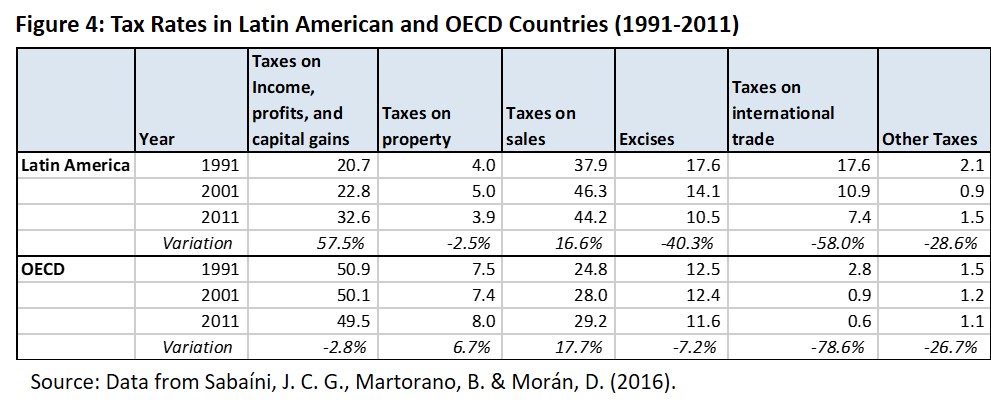

Third, tax policy impacts political capital and resources. Some Latin American countries have been reluctant to make unpopular changes to their tax policies, particularly with broadening the income tax base and expanding the progressive tax elements, since politicians fear losing funding and support from wealthier citizens. Despite these concerns, in the early 2000s, Latin America increased the effective rates for income and capital gains (Figure 4).

This trend towards progressivity has continued into 2011 and beyond. Progressive tax policy requires more than a legal or statutory change, and it is a multi-faceted pursuit for developing countries.

Section III: Progressive Tax and Its Redistributive Impact – A Multi-Faceted Analysis

Most Latin American countries have some form of progressive income tax, according to which the higher the income level, the higher the proportion of taxes incurred. In fact, Hanni, Martner, and Podestá (2015) estimated that 90% or more of a country’s income tax was paid by the 20% highest income bracket. They also found that the top decile (10%) pays, on average, only 5.4% of their gross income in the form of income taxes, a much lower effective tax rate relative to other developed countries. While rates range from 25% to 40%, the effective ones incurred by the largest percentage of tax-paying citizens are much lower, which limits the redistributive effect of income taxes.

Social Impact

The tax burden is a continued sociological debate for developing and developed countries, which is largely influenced by the extent of the willingness of its citizens to be taxed, especially at more progressive rates (Berens & von Schiller, 2017). These beliefs may also be shaped by external societal pressure (Berens & von Schiller, 2017). The concerns over the principal-agent problem, namely, questions regarding how governments will use tax revenue, continue to evolve in developing countries (Berens & von Schiller, 2017). The development of a progressive income tax system is paramount to creating a society of citizens that supports equity, fairness, and social responsibility. Such social factors impact the development of a country’s reputation and collective ideology for sociological sustainability, particularly as progressive taxation can mitigate social tension and distributive conflict.

Political Impact

High inequality may reflect the failure of fiscal policy to perform one of its classical fiscal functions: redistribution (Goñi, López & Servén, 2011). This pursuit from the government sector assumes a certain amount of political capital and stability. Even if addressing such income disparities can create more harmonious civil and political societies, sustained efforts require political structures that can withstand the impacts of redistribution and the reallocation of resources (Tsounta & Osueke, 2014). As more Latin American countries enter contested elections in 2018, the opportunity for adopting more progressive income tax structures becomes both a potential and an aspiration, depending on the country’s current economic and social environments (Berens & von Schiller, 2017).

Economic Impact

According to the World Bank, Latin America ranks among the highest in terms of inequality (Goñi, López & Servén, 2011). This inequality contributes to higher poverty, market imperfections, and institutional constraints, each of which “can be a powerful drag on development and prosperity” (Goñi, López & Servén, 2011). Bird (2008) acknowledged the economic constraints for imposing more progressive tax policy. The largely informal economy within Latin American countries both affects compliance and administration, and demands progressivity as well as the redistribution of resources. For example, wage withholding accounts for 90% of tax revenue in these countries, but their large shadow economies operate outside the formal tax systems (Bird & Zolt, 2011). While the implementation of more progressive tax policies may encourage businesses to enter or persist in the informal sector, the beneficial stability of joining the formal economy can outweigh the costs of additional tax administration and compliance.

Technological Impact

Scholars recognize the technological constraints for the administration of increasingly progressive tax policy, but few experts have analyzed the opportunities to use emerging technology to aid in these administrative efforts (Peccarelli, 2016). This infrastructure presents an opportunity for developing countries to address tax evasion and avoidance, allowing for increased compliance and streamlined costs. Such changes minimize prior concerns by international scholars and local politicians that have contributed to the lack of socio-political support for expanded progressive tax reform in developing countries (Bird & Zolt, 2011). By leveraging technological resources from developed countries, such as satellite imaging, drone- based surveillance, and big data analysis, developing countries can ease administrative burdens towards promoting more robust and progressive tax systems (Peccarelli, 2016). The use of technology to address income redistribution and progressive tax policy warrants additional research.

Legal Impact

A separate revenue authority is one proposed solution and step towards more effective administration and increased compliance (Bird & Zolt, 2008). Local corruption affects implementing tax policy based on fairness and equity, undermining citizens’ confidence in the system, affecting their willingness to pay and reducing the country’s capacity to collect and distribute its tax revenue (Bird & Zolt, 2008). By implementing enforceable progressive tax policy coupled with strong property rights and existing legal infrastructure, Brazil serves as an example for other Latin American countries (Langer & Phillips, 2014).

Conclusion

In developing countries, income inequality plays an important role in creating political and economic instability, as well as suppressing gross domestic product and economic growth. By examining the social, political, economic, technological, environmental, and legal factors that both help and hinder the success of such policies, we discovered some potential tax reforms to improve the income tax’s progressivity. These reforms also may require additional social, political, legal, and technological change. Local and foreign persons and institutions must collaborate to ensure that progressive tax policy be implemented and enforced in developing countries, especially in Latin America, where income inequality may limit economic growth, contribute to political instability, and enhance poverty conditions. Progressive tax reform is a historically underutilized fiscal policy tool, but informed persons should demand structural changes to the distribution of income, starting at the local level and adopting these potentially beneficial policy changes across the developing world.

References

Agarwal, Prateek (2017). The lorenz curve and gini coefficient. Intelligent Economist.

Berens, S. & von Schiller, A. (2017). Taxing higher income: What makes high-income earners consent to more progressive taxation in Latin America? Polit Behav, 39, 703.

Bird, R. M. (2008). Tax challenges facing developing countries. Annual Public Lecture Series of the National Institute of Public Finance and Policy. New Delhi: India.

Bird, R. M. & Zolt, E. M. (2005). Redistribution via taxation: The limited role of the personal income tax in developing countries. UCLA Law Review, 52, 1627-1695.

Bird, R. M. & Zolt, E. M. (2008). Tax policy in emerging countries. Environment and Planning C: Government and Policy, 26, 73-86.

Bird, R. M. & Zolt, E. M. (2011). Dual income taxation: A promising path to tax reform for developing countries. World Development, 39(10), 1691-1701.

Chu, K., Davoodi H. & Gupta, S. (2000). Income distribution and tax and government social spending policies in developing countries. IMF Working Paper, WP/00/62.

Goñi, E., López, J.H. & Servén, L. (2011). Fiscal redistribution and income inequality in Latin America. World Development, 39(9), 1558-1569.

Gordon, R. & Li, Wei (2009). Tax structures in developing countries: Many puzzles and a possible explanation. Journal of Public Economics, 93, 855-866.

Hanni, M., Martner, R. & Poestá, A. (2015). The redistributive potential of taxation in latin america. CEPAL Review, 116, 8-26.

Haughton, J. & Khandker, S. R. (2009). Handbook on poverty and inequality. Washington, DC: The World Bank.

Kalf, J. (2015). Latin America: Progress through populist policies? A mixed picture. RaboResearch, retrieved from www.rabobank.com/economics.

Langer, W. & Phillips, J. (2014). Business and legal considerations for entering international markets: United States and Latin America. Retrieved from http://joelwp.com/2014/11/21/business-and-legal-considerations-for-entering-international-markets-united-states-and-latin-america/.

Lustig, N. (2016). Inequality and fiscal redistribution in middle income countries: Brazil, Chile, Colombia, Indonesia, Mexico, Peru and South Africa. De Gruyter, 7(1), 17-60.

Peccarelli, B. (2016). Tax tech helps developing nations play on the global stage. Thomson Reuters, retrieved from https://blogs.thomsonreuters.com/answerson/tax-tech-helps-developing-nations/.

Piketty, T. (2014). Capital in the twenty-first century. Cambridge: The Belknap Press of Harvard University Press.

Sabaíni, J. C. G., Martorano, B. & Morán, D. (2016). Taxation and inequality: Lessons from Latin America. In International Social Science Council (Ed.), World Social Science Report (pp. 206-211). Paris, France: UNESCO.

Tanzi, V. & Zee, H. H. (2000). Tax policy for emerging markets: Developing countries. National Tax Journal, 53(2), 299-322.

Tsounta, E. & Osueke, A. I. (2014). What is behind Latin America’s declining income inequality? IMF Working Paper.