IBI case #1: The name is bonds, corporate bonds

By Nadia Zaman, Two Year MBA ’19

The first day back from winter break was an adjustment for me; especially getting off a red-eye flight from California and being immersed in 10-degree weather! But it was nice to be back amongst my Johnson MBA friends with an internship in hand. Recruiting was checked off my list leaving me to focus on having a social life and mingling outside of bankers. I thought to myself, ‘this semester will definitely be less intense than the first semester.’ Boy was I wrong. The first Investment Banking Immersion (IBI) case was emailed at 8 a.m. on Monday. Drew Pascarella, lecturer of finance, does not waste a single second.

Before reading the case, my friends and I assumed it would be easy since it was the first one. Our rationale being that professors know students are still in winter-break mode during the first week back. Not Drew. He assigned a bond case, essentially asking us to determine how the bridge loan for United Technologies Rockwell acquisition is going to be financed. We were to create a 10-slide PowerPoint presentation detailing the current environment in investment grade and high-yield bond markets and the structure of the bonds (every little detail such as amount, tenor, tranches, pricing) that we were recommending.

During our first meeting, my teammates looked at each other in confusion—and in semi-freak-out mode. Questions we fired away to each other:

- How should we start?

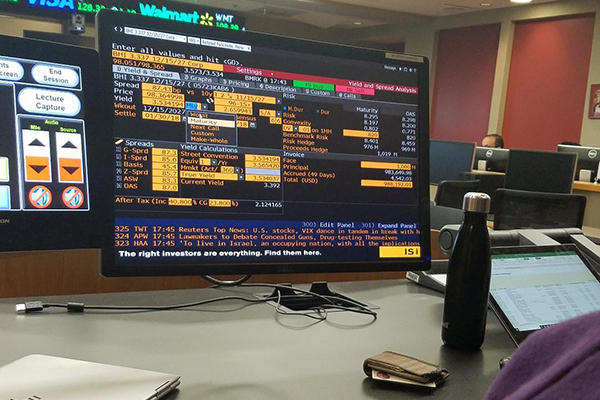

- Should we go on Bloomberg? Capital IQ? FactSet? Thomson Reuters? Barclays Live?

- Does anyone even know how to use any of these programs?

The team decided to play around with Bloomberg and Barclays Live to see if we could get a sense of the bond market. It took me a good hour to find the page that I was looking for, but if it was not for me searching every single function on Bloomberg, I would not know what the Bloomberg terminal is capable of. It was interesting to see what my teammates were capable of, too. One individual was experienced in Thomson Reuters while another was strong in Barclays Live. Teamwork played a big role in getting good progress on our case. Being able to leverage each other’s strengths and learning from one another was key to a successful project.

After we played around on the applications to get a sense of the corporate bond market, we each researched the acquisition of Rockwell Collins by United Technologies (UTX).

My findings included the following:

- United Technologies announced on 9/4/17 it would acquire Rockwell for $30.3 billion, paying $140/share in cash and stock which represented a 25% premium to Rockwell’s unaffected share price as of 8/2/17.

- The deal rationale was that the combined company would generate a run rate of $500 million of synergies (representing 6% of sales) by year four after closing.

- The two businesses are highly complementary to each other, helping with the integration and creation of digital connected planes.

- As part of the transaction, United Technologies received a $6.5 billion 364 days unsecured bridge loan facility.

This is what we had to investigate:

- How many tranches of bonds should be issued and the amount and tenor of each. We did research on recent investment grade bond issuances and what an average amount and tenor was. We narrowed it down to the aerospace and defense industry to see if there was a trend among bonds being issued.

- If we thought whether the combined company of UTX and Rockwell would result in a credit rating downgrade or remain unchanged.

- UTX had existing debt on its balance sheet, which were maturing within the next 30 years, as well as Rockwell’s debt that it was acquiring. We had to make sure the timing of the newly issued bonds would not clash in the same year of an existing loan or note coming due.

This was our solution:

- $14.4 billion of corporate bonds consisting of $1 billion 3-year notes, $3 billion 5-year notes, $3 billion 10-year notes, $3.4 billion 20-year notes, and $4 billion 40-year notes

- The acquisition would result in a one-notch credit rating downgrade from A- to BBB+.

After submitting our final PowerPoint we were exhausted. It was a good 30 hours of work invested in the case over a five-day period. But I learned a lot. One of my classmates, who will be interning at JP Morgan in the summer, called the Investor Relations team at United Technologies to help him out with the project.

Drew’s teaching style is unique but effective. He doesn’t lecture; he assigns a case and expects you to find the information to determine a sound solution similar to the banking environment. For instance, a managing director (MD) at a firm would never show you how to price a bond. Instead, the MD would tell you to price the bond by a certain date, expecting you to figure it out.

Essentially, Drew is the MD throughout the IBI and MBA students are analysts training to be associates. I personally like this teaching method, since I learn by doing.

Now on to learning about IPOs!