Bridging Finance and Infrastructure

Issue NO. 21

By Otaviano Canuto and Aleksandra Liaplina*

The world economy – and emerging market and developing economies in particular – display a gap between infrastructure needs and its finance. On the one hand, infrastructure investment has fallen far short of what would be necessary to support potential growth. On the other hand, abundant financial resources in world markets have been facing very low long-term interest rates, whereas opportunities of higher return from potential infrastructure assets are missed. A bridge between private sector finance and infrastructure can be built if properly structured projects are developed, with risks and returns distributed in accordance with different incentives of stakeholders.

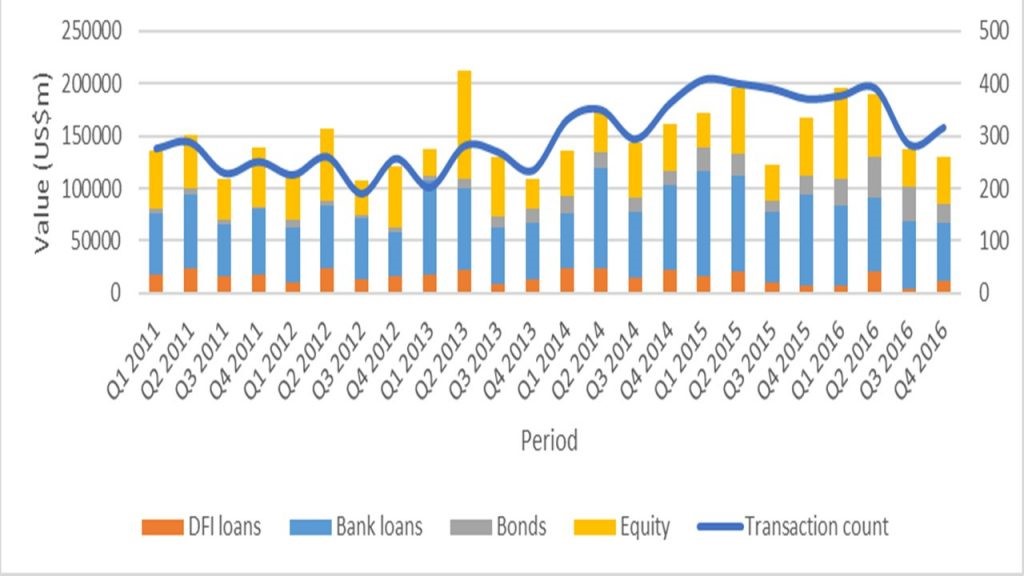

The current infrastructure investment including international financial institutions, public investment and public-private partnerships is around US$1.7 trillion a year, leaving the gap at more than US$1 trillion. Global infrastructure finance has fallen short of its potential – see chart – and institutional investors and other private sector players could increase allocations under appropriate conditions. Leveraging private sector investment, as well as institutional investor capital are widely discussed as possibilities of addressing the needs going forward. Indeed, institutional investors are currently managing assets “exceeding $50 trillion in 2015, compared to $30 trillion in 2007.”

Institutional investors, like all other types of debt and equity investors, have their own incentives, constraints and objectives when it comes to selecting countries, types of projects (“greenfield” vs. “brownfield”) and at what stage of the investment project cycle (development, construction or operation) to invest. Inadequate coverage of risks is named as one of the reasons for projects often not reaching financial close. Defining “attractive investment opportunities” and matching investors to these opportunities in a more systematic way is what might make a difference.

“Heterogeneity in the setup of projects” is often named as one of the reasons for why it is so difficult to push more allocations to infrastructure. Lack of data, different contractual structures, different regulatory environments – all these aspects are part of the puzzle and are being addressed by different players; but also, the breadth of products tailored specifically for different types of institutional investors with their respective risk and return profiles is where a higher effort may payoff. For instance, prospects for institutional investors (e.g. a pension fund) to participate at stages prior to operations become more favorable when refinancing is possible and the construction risk is addressed.

Currency risk is a major factor faced by international investors in emerging markets. Export Credit Agencies can help with that challenge, although often at the expense of higher cost. Other challenges frequently named are the unavailability of financial instruments or their respective cost and complexity in terms of difficulty to use.

Fixed-income instruments such as bonds (in the context of infrastructure project: projects bonds, municipal, sub-sovereign bonds, green bonds and sukuk) and loans (direct/co-investment lending to infrastructure project, syndicated project loans) are likely to be a better fit for the appetite of a broad range of institutional investors in emerging market economies.

Development financial institutions can offer a core financial additionality by playing a key role as a catalyst, drawing private capital into long-term projects in countries and sectors where significant development results can be expected, while the market perceives high risks. Those institutions contribute their own funding (loans, equity) and/or guarantees, providing partners with an improved creditor status. Bringing partners into specific deals through syndications also generates additional financing. Furthermore, they can support the development of pipelines of investable projects, the scarcity of which is often highlighted as an impediment to a higher commitment by non-banking financial institutions to infrastructure.

A whole set of mechanisms to assign part of risks to a third party through risk transfer and credit enhancement instruments is currently being piloted by development banks. These instruments include guarantees, insurance policies, or hedging mechanisms under which, for a fee, the provider will agree to compensate the concessionaire (or its lenders) in case of default and/or loss due to some specified circumstance.

The contrast between the dearth of investments in infrastructure and the savings-liquidity glut that marks the contemporaneous global economy can be reduced. Lowering legal, regulatory, and policy risks are of the essence. Additionally, the availability of sophisticated, developed financial markets and instruments will help, as they facilitate partnerships among different financial agents to allow each one to carry risks that are closer to their will and capacity. The greater involvement of private investors and the design of economically rational financing structures can not only boost the funding of infrastructure investments but also thereby improve the efficiency and success of infrastructure projects. Building such bridge is within reach.

Global infrastructure finance (including corporate finance) value by source of funding, 2011-2016

Source: Canuto, O. and Liaplina, A., “Matchmaking finance and infrastructure”, Capital Finance International, Summer 2017, p.14-18.

*Otaviano Canuto is an Executive Director and Aleksandra Liaplina is an Economist and Infrastructure Finance Specialist at the World Bank. All opinions expressed here are their own and do not represent those of the World Bank or of those governments Mr. Canuto represents at its Board.

The opinions, beliefs and viewpoints expressed by the various authors in this article do not necessarily reflect the opinions, beliefs and viewpoints of Cornell University and the Emerging Markets Institute, or official policies of the Cornell University and the Emerging Markets Institute

Copyright Statement and Policy: the articles from this series and on the Emerging Markets Institute web site may be freely redistributed in other media and non-commercial publications as long as the following conditions are met. 1) The redistributed article may not be abridged, edited or altered in any way without the express consent of the author and 2) The redistributed article may not be sold for a profit or included in another media or publication that is sold for a profit without the express consent of the author.